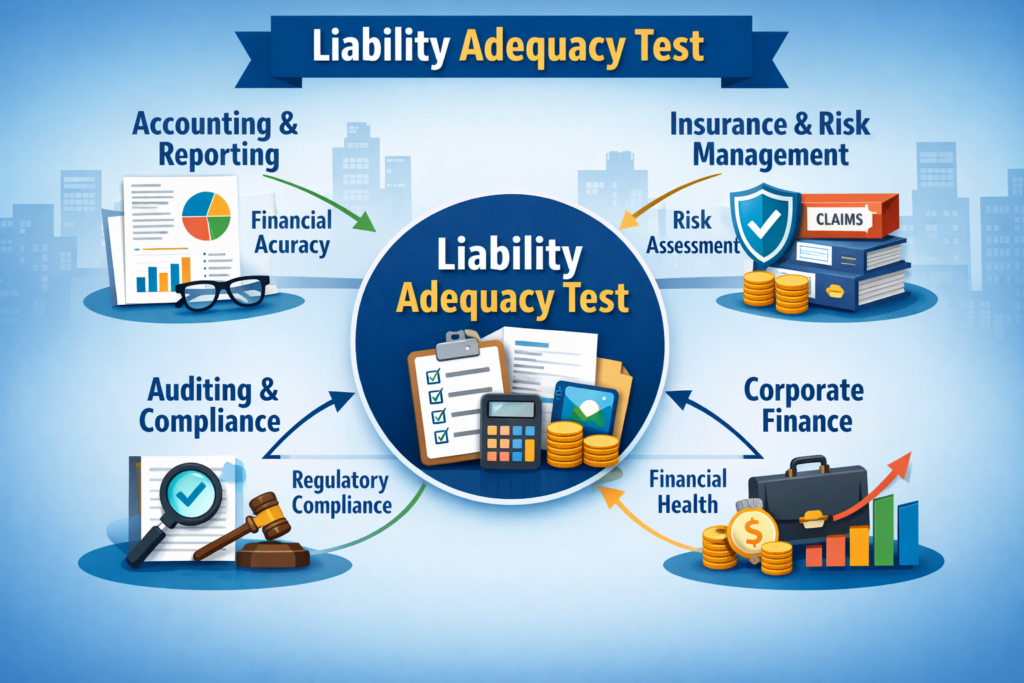

Understanding the Liability Adequacy Test Process

Navigating the world of accounting can be complex, especially

Navigating the world of accounting can be complex, especially when it comes to understanding various financial tests. Among these is the Liability Adequacy Test (LAT), a crucial process that ensures an organization’s liabilities are accurately represented in its financial statements. As businesses strive for transparency and compliance with accounting standards, grasping this test becomes essential.

But what exactly does this test entail? Why is it vital for organizations? Whether you’re an accountant, a finance professional, or simply curious about how companies manage their obligations, exploring the ins and outs of the Liability Adequacy Test will shed light on its importance in maintaining financial health and integrity. Let’s dive into what makes LAT an indispensable part of sound accounting practices.

Understanding the Liability Adequacy Test Process

The Liability Adequacy Test is a systematic evaluation that determines if the liabilities reported by an organization are sufficient to cover future obligations. This process primarily focuses on insurance companies but can apply to any business with long-term commitments.

At its core, the test compares expected cash flows from liabilities against current reserves. By doing so, it assesses whether these funds will be adequate for settling claims or other financial responsibilities.

Carrying out this assessment involves analyzing various factors such as historical claim data, market trends, and economic conditions. Each of these elements plays a pivotal role in predicting future needs.

Understanding the LAT process equips businesses with insights into their fiscal health and promotes informed decision-making. As organizations face changing environments, keeping tabs on liability adequacy becomes increasingly vital for sustainable growth and risk management strategies.

Key Steps in Conducting Liability Adequacy Test

Conducting a Liability Adequacy Test is essential for accurate financial reporting. The process begins with gathering relevant data, including the expected cash flows from insurance contracts. This information forms the foundation of your analysis.

Next, you’ll need to calculate the present value of future cash flows. Using an appropriate discount rate helps ensure that your figures accurately reflect time value considerations.

Once you have these calculations in place, compare the present values against your liabilities. This step identifies whether any additional reserves are necessary or if adjustments can be made.

Documentation plays a crucial role throughout this process. Maintaining clear records aids transparency and supports compliance during audits or reviews.

It’s important to revisit assumptions regularly as market conditions change over time. Adjustments based on updated data keep your tests relevant and reliable in reflecting true liability adequacy.

Importance of Liability Adequacy Test in Accounting

The Liability Adequacy Test (LAT) plays a pivotal role in accounting, particularly for insurance companies. It ensures that an insurer’s liabilities are adequately covered by its assets, safeguarding policyholders’ interests.

By assessing the adequacy of these liabilities, LAT helps identify any potential shortfalls early on. This proactive approach can prevent financial distress and maintain solvency in challenging market conditions.

Moreover, conducting a liability adequacy test fosters transparency and accountability within financial reporting. Stakeholders gain confidence when they see that a company rigorously evaluates its obligations.

Regulatory bodies also emphasize the importance of LAT as it aligns with best practices in risk management. Adhering to these standards not only promotes stability but also enhances the reputation of financial institutions.

Firms that prioritize this test demonstrate their commitment to sound governance and responsible fiscal management.

How to Perform a Liability Adequacy Test

Performing a Liability Adequacy Test is crucial for ensuring that your insurance liabilities are appropriately valued. Start by collecting the necessary data on policyholder benefits and future claim payments. This information will serve as the foundation of your analysis.

Next, assess the adequacy of your reserves. Compare them to expected future cash flows from policies in force. If there’s a shortfall, it indicates that adjustments may be needed to account for potential liability increases.

Utilize statistical methods or actuarial models to project future obligations accurately. These models should factor in various scenarios including changes in mortality rates and economic conditions.

Document every step taken during this process meticulously. Clear documentation aids compliance efforts and provides transparency when presenting findings to stakeholders or auditors.

Liability Adequacy Test: Rules and Guidelines Explained

The Liability Adequacy Test is governed by a set of rules and guidelines that ensure consistency and accuracy in financial reporting. This test is primarily used to assess whether the recognized liabilities are sufficient to cover future claims.

One key guideline involves the use of relevant assumptions about future cash flows. These projections should reflect realistic expectations based on historical data, industry trends, and other pertinent information. Another important consideration is the discount rate applied during calculations. The choice of this rate can significantly impact the present value of expected cash flows.

Additionally, firms must adhere to accounting standards such as IFRS 17 or ASC 944 when conducting these tests. Compliance with these frameworks not only enhances credibility but also facilitates comparability across different organizations.

Documentation plays a critical role as well. Clear records detailing methodologies, assumptions, and outcomes help maintain transparency throughout the audit process.

Regular reviews are essential for ensuring that estimates remain valid over time as market conditions change or new information becomes available. By following these rules and guidelines diligently, businesses can effectively manage their liability exposure while providing accurate financial statements that shareholders trust.